As we wrapped up November across the Truckee and North Lake Tahoe markets, the seasonal rhythm of mountain living made its annual return; ski resorts are spinning lifts, fireplaces are working overtime, and the real estate market is easing into its winter stance. But make no mistake: quieter does not mean stagnant. In fact, beneath the snow-dusted slowdown sits a market that is still adjusting to new buyer psychology, changing economic cues, and a post-pandemic reset that continues redefining what “normal” looks like in our mountains.

Sales Activity & Market Pace

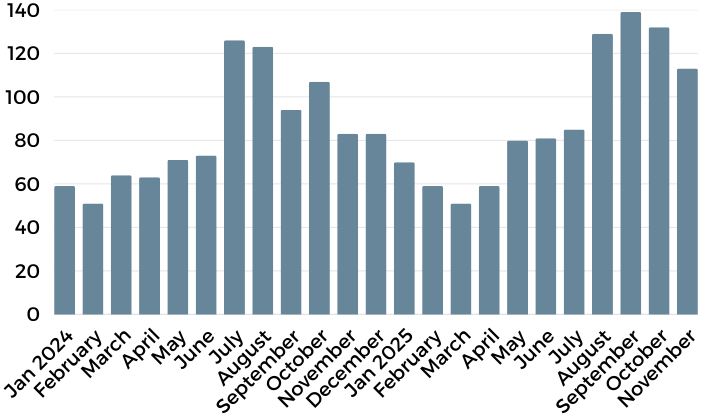

November finished with 113 total sales, marking a 14% decline from October’s 132 closings, a predictable shift as winter logistics, holiday travel, and market fatigue set in. Yet, the bigger picture reveals a far more compelling narrative: sales are up 36% year-over-year, compared to just 83 transactions in November 2024. That surge signals regained buyer engagement and renewed confidence, just not the kind expressed through bidding wars or rushed offers.

Month-over-Month Total Sales Transactions

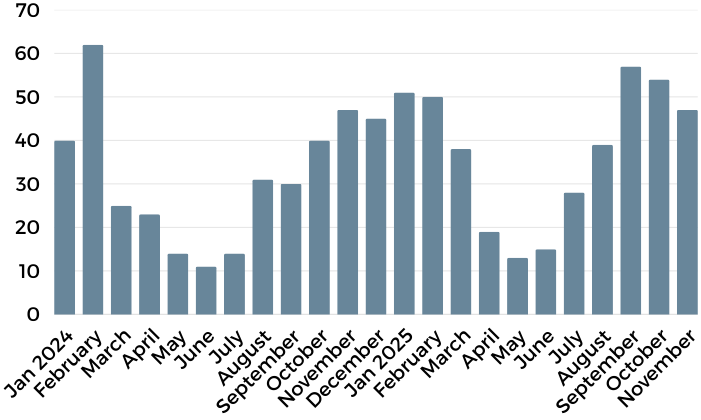

One of the most telling metrics this month: median days on market finally dipped back down, sliding from 54 days in October to 47 days in November, exactly matching last year. That subtle but meaningful move indicates that motivated buyers are striking when they find the right opportunity.

Median Days on Market

Pricing & Value Trends

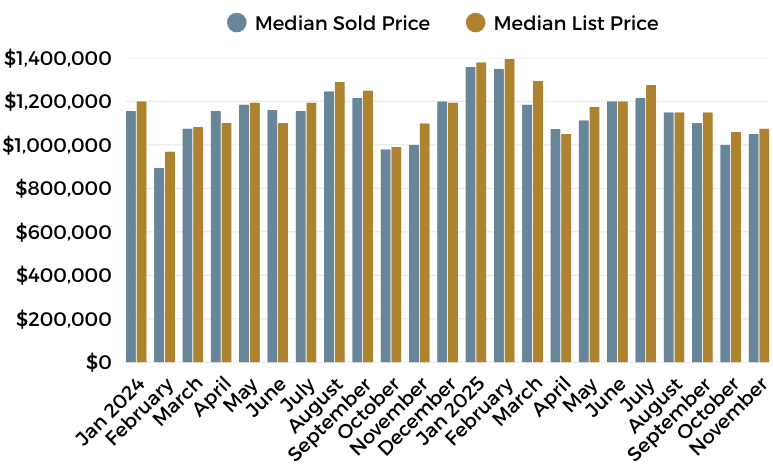

Pricing continues to demonstrate resilience. The median sold price ticked up 5% month-over-month to $1,000,000, matching a modest but steady 5% increase from this time last year. These incremental shifts reflect a market that isn’t overheated, but isn’t softening either. Instead, we’re observing a measured equilibrium: sellers still expect meaningful value, and buyers will absolutely pay it, if the property checks the boxes.

Month-over-Month Sold to List Prices

Negotiations tightened further in November with homes selling at an average of 2.3% below list price, emphasizing a market where pricing accuracy and emotional alignment matter more than ever. Overpriced listings are sitting. Well-priced, well-positioned homes are still moving, just without the frenzy.

Inventory & Market Balance

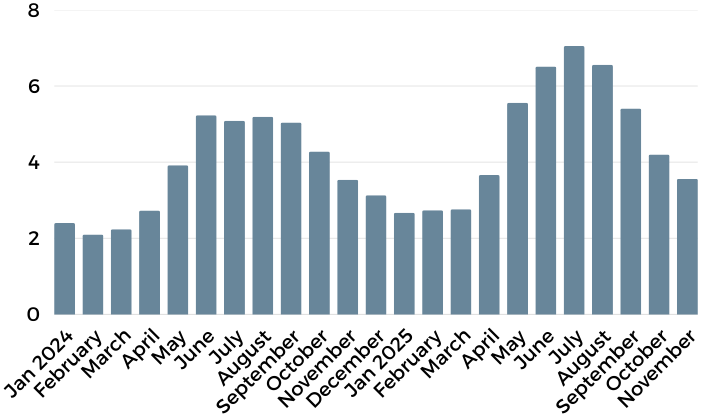

Inventory followed its seasonal downward trajectory, dropping 15% from October and settling at 3.56 months of supply, essentially unchanged from last year at this time. That level keeps the market balanced, but with a slight lean toward sellers as we head into a period when fewer homes typically hit the market.

Months of Inventory

The luxury segment across Truckee and North Lake Tahoe continued its steady normalization in November, following several months of recalibration after years of pandemic-era volatility. Buyer behavior remains calculated rather than reactive, with well-priced, updated, and lifestyle-aligned properties securing offers while anything aspirationally priced continues to sit. Days on market are longer across most communities compared to late summer, yet values remain resilient, showing that while urgency has faded, demand for high-quality mountain homes has not. Across the board, we’re seeing something consistent: buyers will write when the home justifies the price, and sellers aligned with current expectations are the ones successfully closing.

51 sales <$1M

62 sales >$1m

17 sales >$2m

3 sales >$5M

1 Sales >$10M

Martis Camp

Martis Camp recorded one sale in November, trading at a premium $2,146 per square foot, consistent with recent quarters. This reflects Martis Camp’s continued position as the most exclusive and price-secure luxury enclave in the region. While activity has slowed from the peaks of late summer, pricing stability remains a defining feature here, proof that scarcity, design excellence, and lifestyle continue to protect value. Serious buyers remain highly engaged, just more selective and slower to write.

Lahontan

Lahontan had a record breaking month, 130 James Reed closed at $7,850,000, making it the highest sale ever recorded in the community. In total, the community recorded three sales in November, with price-per-square-foot ranging from $804 to $1,308, a meaningful spread that reflects a more discerning buyer pool. Over the last several months, Lahontan pricing has remained stable, but buyers are clearly prioritizing turnkey condition, modern design, and homes with updated finishes. Homes requiring upgrades are taking longer to move and continue to sell with negotiation applied. Lahontan remains one of the most consistent performers in the luxury category, but the days of premium pricing simply based on the address alone are firmly behind us, the value must match the ask.

Gray’s Crossing

Gray’s Crossing saw the strongest sales velocity this month with four closings, continuing its trend as one of the most active luxury communities this fall. Price performance ranged meaningfully, with sold price per square foot landing between $667 and $972, driven by build year, finishes, and location within the community. Compared to the last few months, pricing continues edging higher, particularly for new construction, which continues commanding a premium. The community is benefitting from a mix of modern builds, golf-adjacent lifestyle appeal, and relative affordability compared to Martis Camp and Lahontan. DOM remains moderate, but homes that are dialed-in are moving faster than they were earlier this year. Of note, 10956 Ryley Court closed off market, all cash, for $3.2M.

Old Greenwood

Old Greenwood posted one sale this month at $687 per square foot, a stable result aligned with recent sales. 13490 Fairway Drive closed off market, all cash, for $3.2M. The community continues to draw buyers who value resort-style living and affordability, relative to upper echelon communities like Schaffer’s Mill and Lahontan. Like neighboring luxury communities, the buyer mindset remains measured but engaged.

Northstar Village

Northstar Village also posted three sales this month, with a strong price-per-square-foot range from $937 to $995. This segment continues benefiting from ski-season momentum, and pricing has held firm heading into winter. Compared to September and October, activity tapered slightly, but demand remains steady for units with proximity to lifts and recent renovations. As we move deeper into ski season, we expect energy around Northstar Village inventory to increase, particularly among buyers seeking ease, rental value, and lock-and-leave convenience. Of note, Big Horn 406 closed all cash and $150K below asking down to $1.8M. Of interest, there have been 6 three bedroom condos sales YTD, all but one have received 6 figure price concessions This likely demonstrates seller flexibility in the midst of an evolving Village condo insurance landscape, essentially only allowing cash deals.

Northstar Homes

Northstar Homes had one closing, selling at $542 per square foot, lower than recent months. This is reflective of buyer sensitivity when homes require upgrades or lack modern amenities. Compared to the fall trend line, this sale underscores what we’ve been seeing: homes in this community will sell, but pricing must be aligned with current buyer expectations, not last year’s sentiment.

Incline Village / Crystal Bay Market Update

November brought a noticeable shift to the Incline Village real estate market as the community transitioned toward winter activity and buyers adopted a more measured, evaluation-driven approach. The median sales price rose 23.3% year-over-year to $1,480,000, signaling continued demand for premium lakefront and lifestyle-driven properties. Month-over-month, however, pricing dipped 19.8%, a reflection of smaller sample size and seasonality rather than weakening fundamentals. Closed sales slowed to 20 transactions, down 23.1% from October and 4.8% below last November, highlighting the selective buyer mindset playing out locally and nationally. Meanwhile, homes took significantly longer to sell, with the median days on market jumping to 132—up 43.5% year-over-year and 34.7% from last month, reinforcing the clear message: buyers remain engaged, but only on their terms.

Inventory dynamics are also evolving. While new listings dropped 41.9% month-over-month to just 18, total active inventory remains elevated at 151 homes, still 12.5% higher year-over-year and contributing to a 7.5-month supply of inventory, a level favoring buyers and negotiation. Sellers received an average of 95.6% of list price, nearly flat month-over-month and just 0.1% below last year. That consistency demonstrates willingness from both sides to find alignment when value is clear. And with the median sold price per square foot climbing 7.8% from October and now sitting at $778, the market continues to reward homes with quality condition, amenities, and prime positioning, particularly those delivering turn-key access to skiing, lake recreation, and Nevada’s tax advantages.

As interest rates show signs of long-term stabilization and economic sentiment cautiously improves, Incline Village is entering a rare phase where patient buyers have leverage, and strategic sellers still command premium pricing. Winter is historically a time for quieter transaction volume, but also for meaningful opportunity. The data confirms what many of us feel in real time: the Incline Village market isn’t cooling, it’s recalibrating. And those who understand the nuance are well-positioned heading into 2026.

Looking Ahead: Winter, Optimism, and the Shift That Isn’t Just About Data

While the numbers paint a picture of stability, the sentiment on the ground tells a more nuanced story.

Buyers today aren’t racing. They’re evaluating. They’re thoughtful. And above all, they want to feel like they’re winning. The days of emotionally charged bidding wars are long gone; today’s buyers want logic, value, and alignment with long-term goals. Meanwhile, sellers willing to meet this reality, rather than resist it, are the ones closing escrows.

As we transition fully into winter, the timing for buyers becomes notably appealing: fewer competing buyers, motivated sellers, and the ability to settle in before peak ski months make the idea of waking up slope-side far more than theoretical.

Economically, early forecasts for 2026 point toward gradually improving interest rates, steady demand for vacation and lifestyle properties, and a consumer mindset shifting from hesitancy to selective confidence. In other words: momentum is forming, just quietly.

Final Thought

If the last few years taught us anything, it’s that the Truckee–North Lake Tahoe real estate market doesn’t follow national trends, it writes its own script. And right now, we’re entering a chapter where opportunity is disguised as patience.

So whether you’re thinking of selling before the spring thaw or buying while chairlifts are calling, winter may just be the perfect moment to make your move.